Being in the supplier base is not the same as being in the right contracts

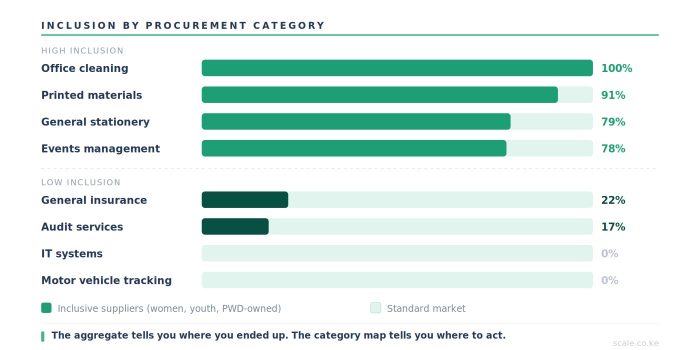

When we run supplier prequalifications, the inclusion data comes out automatically because ownership type is a required field at onboarding. What we see consistently surprises procurement teams – not in the aggregate, but in the pattern beneath it. Women-owned and youth-owned businesses are dominant in some categories. Office cleaning: 100%

When we run supplier prequalifications, the inclusion data comes out automatically because ownership type is a required field at onboarding. What we see consistently surprises procurement teams – not in the aggregate, but in the pattern beneath it.

Women-owned and youth-owned businesses are dominant in some categories. Office cleaning: 100% inclusive. Printed materials: 91%. Events management: 78%. In others – audit services: 17%. Insurance: 22%. Motor vehicle tracking and IT systems: 0%.

The natural reading of that data is that inclusion is uneven across the supply base. Which is true. But there is a harder reading. One that most supplier diversity conversations avoid.

The categories where inclusive businesses are dominant are not equivalent to the categories where they are absent. They are not the same kind of work, the same kind of contract, or the same kind of economic outcome for the businesses that win them.

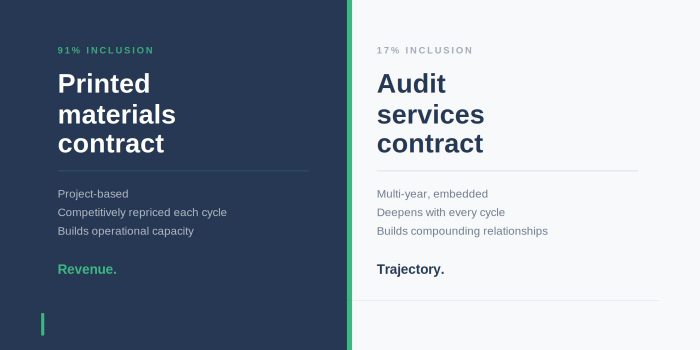

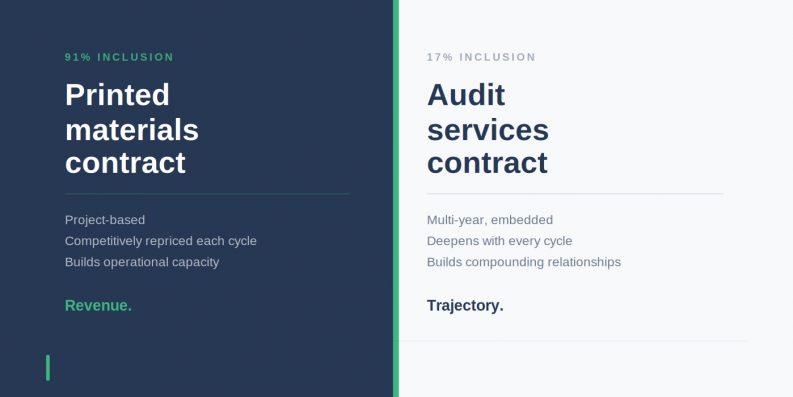

Two contracts. Two trajectories.

A printed materials contract and an audit contract are not the same thing. Both are real work. Both matter. But they are not equivalent economic outcomes for the businesses that win them.

A printed materials contract is typically project-based, competitively repriced each cycle, and won on price and turnaround. The business that wins it earns revenue and builds operational capacity. But it does not necessarily earn the kind of reference that compounds – the embedded relationship, the institutional knowledge, the track record that makes the next contract in a different category easier to win.

The audit contract is typically multi-year and self-reinforcing. Once a firm is the auditor, it is the auditor. The relationship deepens over time. The firm builds knowledge of the client’s governance, its risks, its internal workings. That knowledge is an asset that carries into the next engagement, and the one after that. The economic distance between the two is not just a difference in value. It is a difference in trajectory.

A supplier diversity programme that achieves 91% inclusion in printed materials and 17% in audit is reporting two very different realities inside the same aggregate. Both numbers are real. The aggregate does not distinguish between them.

Why the pattern is structural, not accidental

Here is what the data shows when you look at it honestly.

The categories where women-owned and youth-owned businesses are most present in procurement markets are, without exception, the categories with the lowest barriers to entry, the shortest contract durations, the lowest average contract values, and the least likelihood of compounding into a long-term supplier relationship.

This is not a coincidence. It is a structural pattern. These businesses entered those categories because those categories were accessible. The barriers to entry – capital requirements, professional certifications, prior corporate references, bid bonds – were low enough to clear. They competed. They won. They are there.

The categories where they are absent are not categories where inclusive businesses do not exist or cannot compete. Women-owned audit firms exist in Kenya. Youth-owned technology companies exist. The absence is not about capability. It is about access.

The prequalification criteria in a high-value professional services category typically require three years of audited financials, a minimum annual turnover threshold, prior experience with clients of a comparable size, and professional body membership. Each of those requirements is individually defensible. Together, they describe a category that has been designed – not deliberately, but effectively – to select for incumbents.

An incumbent does not need to declare its ownership type. It does not need to compete on diversity credentials. It has the reference, the relationship, and the panel position it built before any of this was a conversation. The system was never designed to exclude women-owned or youth-owned businesses. It was designed for convenience. The exclusion is a consequence, not an intention. But the consequence is real.

Participation is not the same as advancement

This matters because of what supplier diversity programmes are actually for.

If the goal is to report a number – to show a board or a donor or a regulator that a percentage of procurement spend reached preferred supplier groups – then the aggregate is sufficient. Include enough cleaning contracts and the aggregate looks fine. This is not dishonest, exactly. But it is not the point.

If the goal is economic advancement – if the programme exists because there is something unjust about who gets access to corporate procurement markets and who does not – then the aggregate is not sufficient. Because a printed materials contract and an audit contract are not equivalent instruments of economic advancement. Both pay the bills. But one builds a compounding business relationship and the other does not. That difference is what a diversity programme exists to address.

The question a genuinely strategic supplier diversity programme should be asking is not “what is our overall percentage?” It is “which categories are we actively opening to businesses that were not previously in them, and what is the contract value of those awards?”

Those are different questions. The second one is harder. And the second one is the one that matters.

The data that changes the question

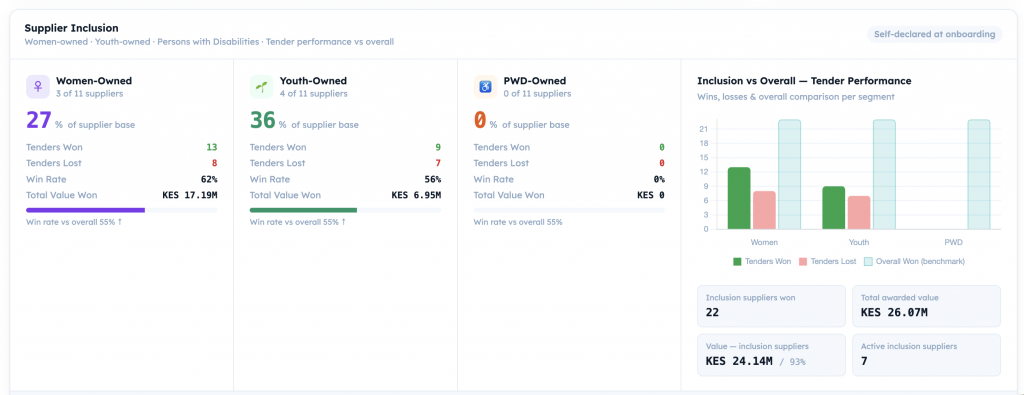

I do not think most organisations ask the second question because they do not have the data to answer it. Not because they are not interested. Because the data – category-level win rates, contract values by supplier group, participation trends across RFx cycles – is not something most procurement systems produce. It has to be deliberately built.

What Scale tracks, for every RFx that runs through the platform, is not just whether inclusive suppliers were in the panel. It is whether they were invited, whether they responded, whether they won, and what the contract was worth. By category. By supplier ownership group. By quarter.

That data produces a different picture from the aggregate. It shows which categories are genuinely open and which have inclusion on paper but not in practice. It shows whether the win rate for women-owned businesses in a given category is improving or static. And it shows whether the contract values being awarded to inclusive suppliers are concentrated at the bottom of the spend distribution or distributed across it.

The category map tells you where the gap is. That data tells you whether you are closing it.

A category strategy, not a diversity target

The practical implication is not that organisations should stop counting cleaning contracts. Every contract matters. Every business that wins work through a structured procurement process is in a better position than one that did not.

The implication is that an organisation serious about supplier diversity needs a category strategy, not just a diversity target. It needs to identify the high-value categories where inclusive businesses are underrepresented, understand specifically what is blocking them, and deliberately redesign the access point.

Sometimes that means adjusting the turnover threshold in a prequalification. Sometimes it means removing the bid bond requirement for contracts below a certain value. Sometimes it means splitting a large contract into smaller lots that a growing business can actually bid for. None of these are radical interventions. They are design decisions that require someone to look at the category map and ask: why does this look the way it does, and what would it take to change it?

That question does not get asked when the aggregate looks fine.

From counting to strategy

Supplier diversity reporting has matured considerably in the last five years. Organisations are measuring more, disclosing more, and being held to account more. That is good.

The next maturation is from counting to strategy. From reporting participation to measuring advancement. From asking “how many” to asking “which categories, at what value, with what trend.”

The aggregate will always look better than the category map. That is the point of looking at the category map.